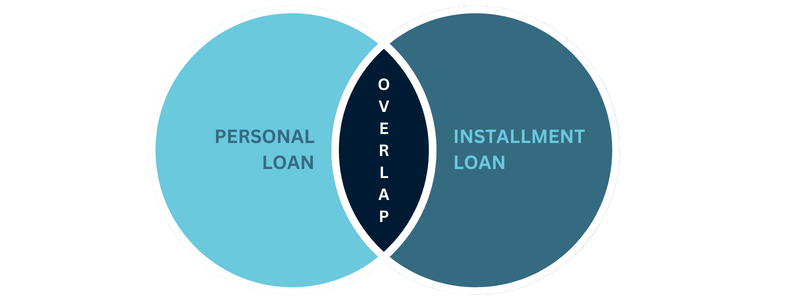

If someone told you that personal loans are installment loans, but installment loans aren’t always personal loans, would you understand? The world of finance, and the terminology used within it can be confusing. But to stand the best chance of financial success, it’s critical to understand the differences. Knowing what loan type is right for your situation could save you in the long run.

What Are Installment Loans?

As mentioned above, a personal loan is an installment loan, but an installment loan isn’t necessarily a personal loan. Installment loans are any type of loan with a set number of payments to repay it. Because of that broad definition, you can think of installment loans like an umbrella. That umbrella covers mortgages, car loans, and personal loans; but each loan type varies in the specifics. These loans are almost always paid back through equal payments across a weekly, biweekly, or monthly payment schedule. Beyond that, the loan can vary drastically based on the personal information and credit history of the individual applying.

Personal Loans vs. Installment Loans

Which One to Choose

Personal loans and installment loans can both be used for a wide variety of purposes. From debt consolidation or medical emergencies, to vacations, and everything in between. For standard financial needs either type of loan will suffice. Where the two vary is when it comes to bigger, more specific needs like purchasing a car or a home. Auto loans and mortgages are considered installment loans, but are not personal loans. And should be used accordingly.

While the flexibility of a personal loan would allow you to use your funds towards your car or home purchase, it will likely cost you more to do so. Mortgages and car loans are standalone items for a reason; they are financing solutions tailored specifically to one purpose. Taking out a personal loan to pay for your house or car will almost never result in the best case scenario. Stick to the proper lending avenues for these items and get installment loans through a mortgage broker or auto lender. If down the line you need to do work on your home or car, then look to a personal loan for funding support.

How to Pay Them Back

A loan from either category is almost always paid back through equal monthly or bi-weekly payments. These will be set up with the lender you work with, but can be anticipated to follow a regular payment schedule. The specifics of repayment will vary depending on a number of factors. Your personal financial standing will influence what interest rate the lender offers you as well as how long you have to pay it back.

Secured vs. Unsecured

Personal loans and installment loans often differ in regards to secured vs. unsecured. Personal loans are more often than not unsecured, meaning they don’t require collateral to be placed against the loan. Taking an unsecured loan can therefore result in higher interest rates as there is more risk for the lender. While many installment loans are secured as they usually finance larger purchases, like a home and require collateral.

Should I Take an Installment Loan?

When considering any type of loan, it’s good to ask yourself a few questions before making your decision.

- Do I need this loan, at this time?

- Can I afford the repayment terms of this loan without financial stress?

- What are the repercussions if I cannot pay back this loan?

- Is this the best type of loan for what I’m using the funds for?

Choosing to take an installment loan shouldn’t be different than choosing to take out any sort of financial support. If you answer the questions above and don’t feel confident about the decision, you may want to reconsider if a loan is the right choice. Number four is also crucial to ensure you are taking the best loan type for its intended use. When beginning your loan search and applications, be as specific as possible with all details. This should help you find the best results available to you.

Above all, just be sure to do your research about the loan. Understand all costs and details of the lender and their specific loan process before signing anything. A loan search engine like LoanConnect is a great place to start as you will get results from multiple lenders through one application. Apply for free to get results from multiple lenders across Canada and compare your rates before choosing to proceed. Never rush a decision that can carry so much weight to your financial future.